Crowding Out

The crowding-out effect is the economic theory that public sector spending can lessen or eliminate private sector spending. It's where the government's budget deficit increases demand for loanable funds, but it reduces the amount of available loanable funds for private investors. It increases demand but also increases interest rates. Less investment happening by the private sector means the national economic growth is not happening. This reduces demand and brings the economy back to where it started: a recessionary gap.

**In a sense, crowding out cancels out the effects of an expansionary fiscal policy. **

Looking at the Graph

The federal government is the largest demander for loanable funds. For example, the government just borrowed a good portion of the bank’s loanable funds. You go to the bank for a car loan, however, the interest rate increased because the government owns a large portion of the funds. Demand for the loanable funds increased, so interest rates increased appropriately. You decide not to buy the car because the monthly payments and interest rates are too high. Other people make the same decision as you. This causes the demand for cars to drop and auto workers are laid off.

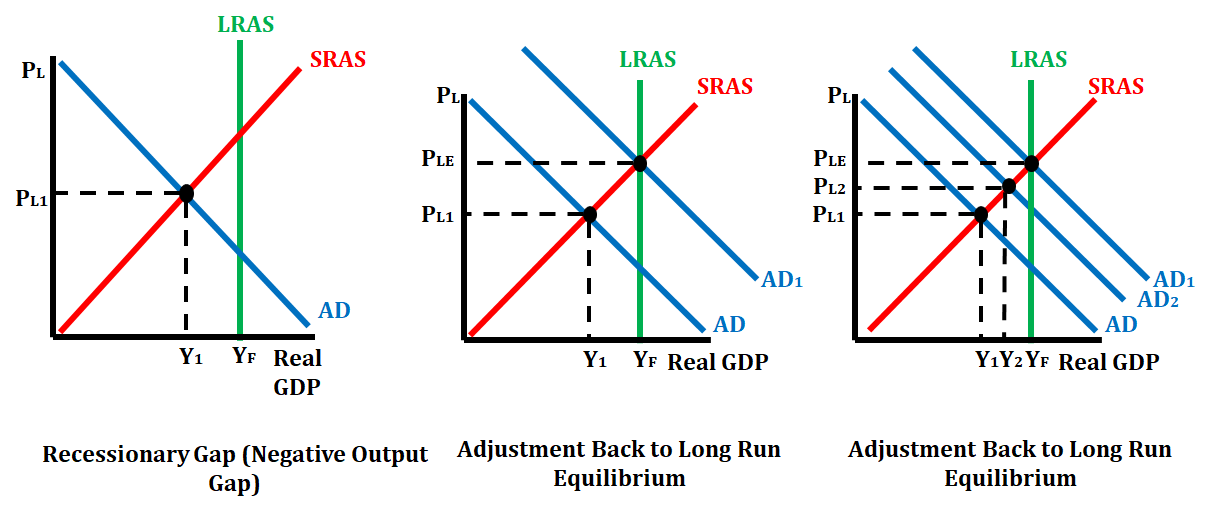

The graph on the left shows an economy in a recessionary gap. The graph in the middle shows the rightward shift of aggregate demand (AD) that can correct a recessionary gap when the government increases its spending in order to get the economy moving again. The graph on the right shows what can happen when crowding out occurs. Instead of government spending correcting the economy, they choose to spend money on a good or service that will decrease or eliminate private spending, causing the economy to move only from AD to AD2. When crowding out occurs, the economy does not quite get back to long-run equilibrium.

Long-Run Impact

Fortunately, crowding out is not always an issue. Sometimes, there will be enough loanable funds for everyone. The government borrows the loanable funds because it is already in a deficit and it goes into a even more deficit in order to save the economy from going into a depression. However, despite its efforts to fight off a looming depression by closing up the recessionary gap, crowding out can cancel out these efforts.

Economy

If this crowding out prolongs for a longer time, we will essentially come into a situation where economic growth is severely reduced. Our economy might start going downhill and widen the recessionary gap because more people are saving instead of spending, thus decreasing demand. This can cause the government to enact an expansionary fiscal policy, only to have it cancelled by crowding out. This can lead to a vicious cycle where the final destination is economic doom.

Infrastructure

Crowding out can have a serious impact on infrastructure too. If private investments decrease due to crowding out, more and more private firms will be discouraged from participating in infrastructure building because of low investment or because of its unprofitable nature. This can lead to a decrease or inefficiency in building things like roads, bridges and hospitals. It can also decrease the quality of the infrastructure as well.

Quick MCQ

The crowding-out effect from the government borrowing is best described as

A. the rightward shift in AD in response to the decreasing interest rates from contractionary fiscal policy.

B. the leftward shift in AD in response to the rising interest rates from expansionary fiscal policy.

C. the effect of the president increasing the money supply, which decreases real interest rates, and increases AD.

D. the effect on the economy of hearing the chairperson of the central bank say that they believe that the economy is in a recession.

E. the lower exports due to an appreciating dollar versus other currencies.

✨

✨

✨

✨

✨

✨

✨

✨

✨

Answer: B. the leftward shift in AD in response to the rising interest rates from expansionary fiscal policy.

Remember, crowding out is the cancelling of expansionary fiscal policy. The cause should be something related to expansionary fiscal policies. That only leaves with the answer B. Plus, it talks about the leftward shifting of AD, which is what happens when crowding-out effects take place. Expansionary fiscal policy shifts AD right, and crowding-out shifts AD left.

Frequently Asked Questions

What is crowding out in economics and why does it happen?

Crowding out is when higher government borrowing (a budget deficit) raises the real interest rate and reduces interest-sensitive private spending—especially investment (EK POL-3.C.1, 3.C.3). In the loanable funds market, a bigger government demand for loans shifts demand right, raising the equilibrium real interest rate and lowering private investment. You can also show this with IS-LM: fiscal expansion shifts IS right, raising interest rates and reducing some of the intended boost to investment. Short run: fiscal stimulus raises AD but partly “crowds out” private investment. Long run: less physical capital accumulation → slower potential GDP growth (EK POL-3.C.4). On the AP exam you should be ready to draw a loanable funds graph or IS-LM/AD-AS to show the effect (Skill Category 4 graphing). Review Topic 5.5 on Fiveable (https://library.fiveable.me/ap-macroeconomics/unit-5/crowding-out/study-guide/s9jP9K7jz7sTI0mO0VYz) and practice more problems (https://library.fiveable.me/practice/ap-macroeconomics).

How does government borrowing affect interest rates and private investment?

When the government runs a deficit it borrows in the loanable-funds market (EK POL-3.C.1 & EK POL-3.C.2). That higher demand for loans shifts the demand curve right, raising the equilibrium real interest rate. Higher real interest rates make interest-sensitive private spending—especially business investment—more expensive, so private investment falls. That adverse effect is called crowding out (EK POL-3.C.3). In the long run less investment can mean slower physical capital accumulation and lower growth (EK POL-3.C.4). On the AP exam you should be ready to show this with a correctly labeled loanable-funds graph (Skill 4—draw and show shifts). For a quick review see the Topic 5.5 study guide (https://library.fiveable.me/ap-macroeconomics/unit-5/crowding-out/study-guide/s9jP9K7jz7sTI0mO0VYz) and the Unit 5 overview (https://library.fiveable.me/ap-macroeconomics/unit-5). Practice applying this to FRQ-style graphs at Fiveable’s practice problems (https://library.fiveable.me/practice/ap-macroeconomics).

Can someone explain the loanable funds market graph for crowding out?

Think of the loanable funds market like any supply/demand graph but for real loanable funds (savings supply on the vertical axis: real interest rate r; quantity of loanable funds on the horizontal axis). When the government runs a deficit it borrows—this is an added demand for loanable funds. So on the graph: - Demand for loanable funds (D) shifts right (D1 → D2). (EK POL-3.C.1, .2) - The equilibrium real interest rate rises (r1 → r2). - The quantity of private investment falls because higher r makes investment projects less attractive—that fall in private investment is “crowding out.” (EK POL-3.C.3) Label initial and new equilibria, r1/r2 and Q1/Q2, and show investment falling. Note: fiscal expansion may be fully or partially crowded out (monetary policy can offset it). You’ll need to draw this correctly on AP free-response questions (graphing is heavily weighted). For a quick review and practice problems, see Fiveable’s Topic 5.5 guide (https://library.fiveable.me/ap-macroeconomics/unit-5/crowding-out/study-guide/s9jP9K7jz7sTI0mO0VYz), the Unit 5 overview (https://library.fiveable.me/ap-macroeconomics/unit-5), and practice questions (https://library.fiveable.me/practice/ap-macroeconomics).

I don't understand how fiscal policy causes crowding out - help?

Crowding out is when higher government borrowing (a bigger budget deficit) raises the real interest rate and reduces interest-sensitive private spending—mostly investment (EK POL-3.C.1, .3). In the loanable funds model: government borrowing shifts demand for loanable funds right → equilibrium real interest rate rises → quantity of private investment falls. You should be able to draw this for FRQs (CED expects the loanable funds market; IS-LM is another option) (EK POL-3.C.2). In the short run that lowers the fiscal multiplier; in the long run less investment means slower physical capital accumulation and weaker growth (EK POL-3.C.4). Note: crowding out isn’t guaranteed if monetary policy offsets higher rates, or if households fully anticipate taxes (Ricardian equivalence). For a clear diagram and practice, use the Topic 5.5 study guide (https://library.fiveable.me/ap-macroeconomics/unit-5/crowding-out/study-guide/s9jP9K7jz7sTI0mO0VYz), the Unit 5 overview (https://library.fiveable.me/ap-macroeconomics/unit-5), and tons of practice problems (https://library.fiveable.me/practice/ap-macroeconomics).

What's the difference between crowding out and fiscal policy effects?

Crowding out is a specific adverse effect that can happen when expansionary fiscal policy (higher G or lower T) is financed by borrowing. In the loanable funds market, bigger government demand for loans raises the equilibrium real interest rate, which reduces interest-sensitive private investment—that reduction is “crowding out” (EK POL-3.C.2, EK POL-3.C.3). “Fiscal policy effects” is broader: fiscal stimulus shifts Aggregate Demand (AD) right, raising real GDP and the price level in the short run (you’ll show this on AD-SRAS or IS-LM graphs on the AP FRQ). Crowding out lowers the net boost to AD because higher interest rates cut private spending; in extreme cases it can largely offset the fiscal multiplier. Long run, persistent crowding out can slow capital accumulation and growth (EK POL-3.C.4). For AP exam free responses, be ready to draw a loanable-funds graph or IS-LM to show how borrowing raises r and reduces I (see the Topic 5.5 study guide: https://library.fiveable.me/ap-macroeconomics/unit-5/crowding-out/study-guide/s9jP9K7jz7sTI0mO0VYz). For more review and practice, check the Unit 5 overview (https://library.fiveable.me/ap-macroeconomics/unit-5) and 1000+ practice questions (https://library.fiveable.me/practice/ap-macroeconomics).

When the government borrows money, why do interest rates go up?

Because the government borrows to cover a deficit, it adds demand for loanable funds. In the loanable funds market that raises the equilibrium real interest rate: with more borrowing demand (or a rightward shift of demand), the price of borrowing—the real interest rate—goes up until supply and demand balance. Higher real interest rates make interest-sensitive private spending (like business investment) more expensive, so private investment falls—that’s crowding out (EK POL-3.C.2 and EK POL-3.C.3). On the AP exam you should be ready to draw the loanable funds graph and show demand shifting right and the interest rate rising; Topic 5.5 study guide covers this (https://library.fiveable.me/ap-macroeconomics/unit-5/crowding-out/study-guide/s9jP9K7jz7sTI0mO0VYz). For extra practice, try the AP Macro practice set (https://library.fiveable.me/practice/ap-macroeconomics).

How do I draw the loanable funds graph showing crowding out effects?

Draw the loanable funds market: vertical axis = real interest rate (r), horizontal = quantity of loanable funds (Q). Start with Supply = S (national saving) upward?—actually S is upward-sloping in some texts but in AP the supply of loanable funds (saving) is upward/steeper; Demand = D (investment + gov borrowing). Step-by-step: 1. Label initial equilibrium where D0 intersects S at r0 and Q0. 2. When the government runs a deficit it borrows, so demand for loanable funds increases: shift D0 → D1 (right). 3. New intersection with S gives a higher real interest rate r1 and larger total Q1. 4. Show “crowding out” by drawing private investment: mark the original private-investment quantity (point on D0 at r1) and show that at r1 private investment is lower than before—private I falls because higher r crowds out interest-sensitive investment. 5. Add labels: “Government borrowing ↑ → D right → r ↑ → Investment ↓ (crowding out).” On the AP exam you must draw and label axes, curves, original and new equilibria, and indicate the change in private investment (Skill 4: Create graphs). For a quick refresher see the Topic 5.5 study guide (https://library.fiveable.me/ap-macroeconomics/unit-5/crowding-out/study-guide/s9jP9K7jz7sTI0mO0VYz) and more practice problems at (https://library.fiveable.me/practice/ap-macroeconomics).

What happens to private investment when the government runs a budget deficit?

When the government runs a budget deficit it typically borrows to finance spending (CED EK POL-3.C.1). In the loanable-funds market that means the demand for loanable funds shifts right, which raises the equilibrium real interest rate (EK POL-3.C.2). Higher real interest rates make interest-sensitive private spending—especially business investment—fall. That fall in private investment is called crowding out (EK POL-3.C.3). In the short run you get less private investment; in the long run that can mean slower physical capital accumulation and lower economic growth (EK POL-3.C.4). You should be ready to show this on the loanable-funds graph (and sometimes with IS-LM on FRQs)—draw demand shifting right, higher r, and a smaller I (investment). For extra review, see the Topic 5.5 crowding-out study guide (https://library.fiveable.me/ap-macroeconomics/unit-5/crowding-out/study-guide/s9jP9K7jz7sTI0mO0VYz), the full Unit 5 overview (https://library.fiveable.me/ap-macroeconomics/unit-5), and practice problems (https://library.fiveable.me/practice/ap-macroeconomics).

Why does crowding out reduce economic growth in the long run?

Crowding out lowers long-run growth because government borrowing raises real interest rates and crowds out private investment. In the loanable-funds model (what the AP expects you to use), a bigger budget deficit shifts the demand for loanable funds right → equilibrium real interest rate rises. Higher rates make interest-sensitive spending—especially business investment in physical capital—fall. With less investment, the economy accumulates capital more slowly, so LRAS (and potential output) grows more slowly over time (CED EK POL-3.C.1–3.C.4). You should be able to show this with a correctly labeled loanable-funds graph on the exam. For a quick review, see the Topic 5.5 study guide (https://library.fiveable.me/ap-macroeconomics/unit-5/crowding-out/study-guide/s9jP9K7jz7sTI0mO0VYz) and the Unit 5 overview (https://library.fiveable.me/ap-macroeconomics/unit-5). For extra practice, check the AP practice questions (https://library.fiveable.me/practice/ap-macroeconomics).

I'm confused about how government spending can hurt the economy through crowding out?

Crowding out means that when the government runs a deficit and borrows more, it pushes up the real interest rate and reduces interest-sensitive private spending (especially investment). In the loanable funds model, government borrowing shifts the demand for loanable funds right → equilibrium real interest rate rises → quantity of private investment falls. Short run effect: fiscal expansion raises AD but some of that is offset because higher interest rates dampen consumption and investment. Long run implication (CED EK POL-3.C.4): less physical capital accumulation → slower potential GDP growth. You can also show this in IS-LM (fiscal expansion shifts IS right → higher r → smaller increase in Y). On the AP exam you should be ready to draw and label a loanable-funds graph (Skill 4: create graphs/visuals). For a concise study guide on Topic 5.5 see Fiveable (https://library.fiveable.me/ap-macroeconomics/unit-5/crowding-out/study-guide/s9jP9K7jz7sTI0mO0VYz) and more practice questions at (https://library.fiveable.me/practice/ap-macroeconomics).

What are some real world examples of crowding out happening?

Crowding out happens when government deficits raise demand for loanable funds, pushing real interest rates up and reducing interest-sensitive private investment (CED EK POL-3.C.2–3). Real-world examples: - U.S. in the 1980s: large federal deficits (Reagan-era tax cuts + spending) coincided with higher real interest rates and reduced private investment—a classic loanable-funds crowding-out story. - Post-2008 stimulus (short term): some economists argued parts of stimulus were partly crowded out as government borrowing competed with private borrowers, though low global savings kept rates muted. - World War II: massive government borrowing redirected funds away from private sector; policy and rationing also affected investment. Caveats: crowding out is smaller when monetary policy offsets rate rises, or when global capital inflows keep rates low; Ricardian equivalence can also limit it. For AP review, link the loanable funds and IS-LM graphs to show how deficit → demand for loanable funds shifts right → higher r → lower I. Review the Topic 5.5 study guide (https://library.fiveable.me/ap-macroeconomics/unit-5/crowding-out/study-guide/s9jP9K7jz7sTI0mO0VYz) and practice problems (https://library.fiveable.me/practice/ap-macroeconomics).

How do I know if a question is asking about crowding out vs regular fiscal policy?

Ask: does the question mention government borrowing raising interest rates and reducing private investment? If yes—it’s crowding out. Key signals: - Wording: look for “budget deficit,” “government borrows,” “loanable funds,” “equilibrium real interest rate,” or “interest-sensitive investment.” Those are CED crowding-out clues (EK POL-3.C.1–3.C.3). - Graph clue: you’ll use the loanable funds market (Dgov shifts right → r rises → I falls). Sometimes IS-LM is used: fiscal expansion shifts IS right, raises r, which reduces planned investment. - If it only asks “what happens to AD, output, and price level” after a change in G or T with no mention of interest rates or private investment, it’s regular fiscal policy (AD shifts)—not crowding out. On the exam, crowding-out questions expect you to show the effect on interest rates and investment (loanable funds or IS-LM graphs). Review the Topic 5.5 study guide (https://library.fiveable.me/ap-macroeconomics/unit-5/crowding-out/study-guide/s9jP9K7jz7sTI0mO0VYz) and practice problems (https://library.fiveable.me/practice/ap-macroeconomics).

What's the connection between budget deficits and crowding out?

When the government runs a budget deficit it borrows in the loanable funds market to finance that gap (CED EK POL-3.C.1). More government demand for loans shifts demand for loanable funds right, raising the equilibrium real interest rate (EK POL-3.C.2). Higher real interest rates make interest-sensitive private spending—especially business investment—more expensive, so private investment falls. That adverse effect is “crowding out” (EK POL-3.C.3). Over time less investment can mean slower physical capital accumulation and weaker long-run growth (EK POL-3.C.4). On the AP exam you should be ready to show this with a loanable-funds graph (or an IS–LM graph on a free-response), label the shift and higher real interest rate, and explain the drop in investment. For a short study review, see the Topic 5.5 crowding-out guide (https://library.fiveable.me/ap-macroeconomics/unit-5/crowding-out/study-guide/s9jP9K7jz7sTI0mO0VYz). For extra practice problems, check (https://library.fiveable.me/practice/ap-macroeconomics).

Does crowding out always happen when the government increases spending?

Not always. Crowding out is what happens when government runs a deficit and borrows in the loanable-funds market, pushing up the equilibrium real interest rate and reducing interest-sensitive private investment (EK POL-3.C.1–3). But the size (or existence) of crowding out depends on things: how much the deficit is, how interest-sensitive private spending is, whether the central bank offsets with monetary policy, and whether households behave like Ricardian agents who raise saving when the government borrows. In an open economy, some of the higher interest rates attract capital inflows, which reduces domestic crowding out. On the AP exam you should show this with a loanable-funds graph (or an IS–LM set-up) and explain partial vs. full crowding out. For a concise review and graphs, see the Topic 5.5 study guide (https://library.fiveable.me/ap-macroeconomics/unit-5/crowding-out/study-guide/s9jP9K7jz7sTI0mO0VYz). For extra practice, try problems at (https://library.fiveable.me/practice/ap-macroeconomics).

How does crowding out affect physical capital accumulation over time?

When the government runs a deficit it borrows in the loanable funds market. That raises the demand for loanable funds, which increases the equilibrium real interest rate. Higher real interest rates make interest-sensitive private investment (like buying new machines or building factories) more expensive, so private firms invest less. Over time that “crowding out” means the economy accumulates physical capital more slowly, so the capital stock grows less and long-run output (and economic growth) is lower than it would be without the deficit. On the AP, you should be ready to show this with a loanable-funds graph (demand for loanable funds shifts right → higher r → lower I) and to explain short-run vs. potential long-run effects (CED EK POL-3.C.2–C.4). For a focused review, see the Topic 5.5 study guide (https://library.fiveable.me/ap-macroeconomics/unit-5/crowding-out/study-guide/s9jP9K7jz7sTI0mO0VYz) and practice problems (https://library.fiveable.me/practice/ap-macroeconomics).